[#title_feedzy_rewrite]

The stablecoin market has witnessed a dramatic surge. These digital currencies are pegged to stable assets like the US dollar. In 2024, they solidified their position as a cornerstone of the Web3 economy. This growth underscores their increasing utility beyond just crypto trading. They are now integral to payments, remittances, and passive income strategies.

Stablecoins Eclipse Traditional Payments: Transaction Volume Soars

The stablecoin market continues its remarkable ascent, firmly establishing itself as a crucial pillar of the Web3 economy. A pivotal highlight from 2024 was the extraordinary $27.6 trillion in total stablecoin transfer volume, which surpassed the combined transaction volumes of Visa and Mastercard. This monumental shift underscores blockchain’s increasing adoption for global payments. This momentum persisted into Q1 2025, with stablecoin transaction volume again outperforming Visa, and Ethereum’s Layer-1 recording a high of $480 billion in stablecoin volume in May 2025.

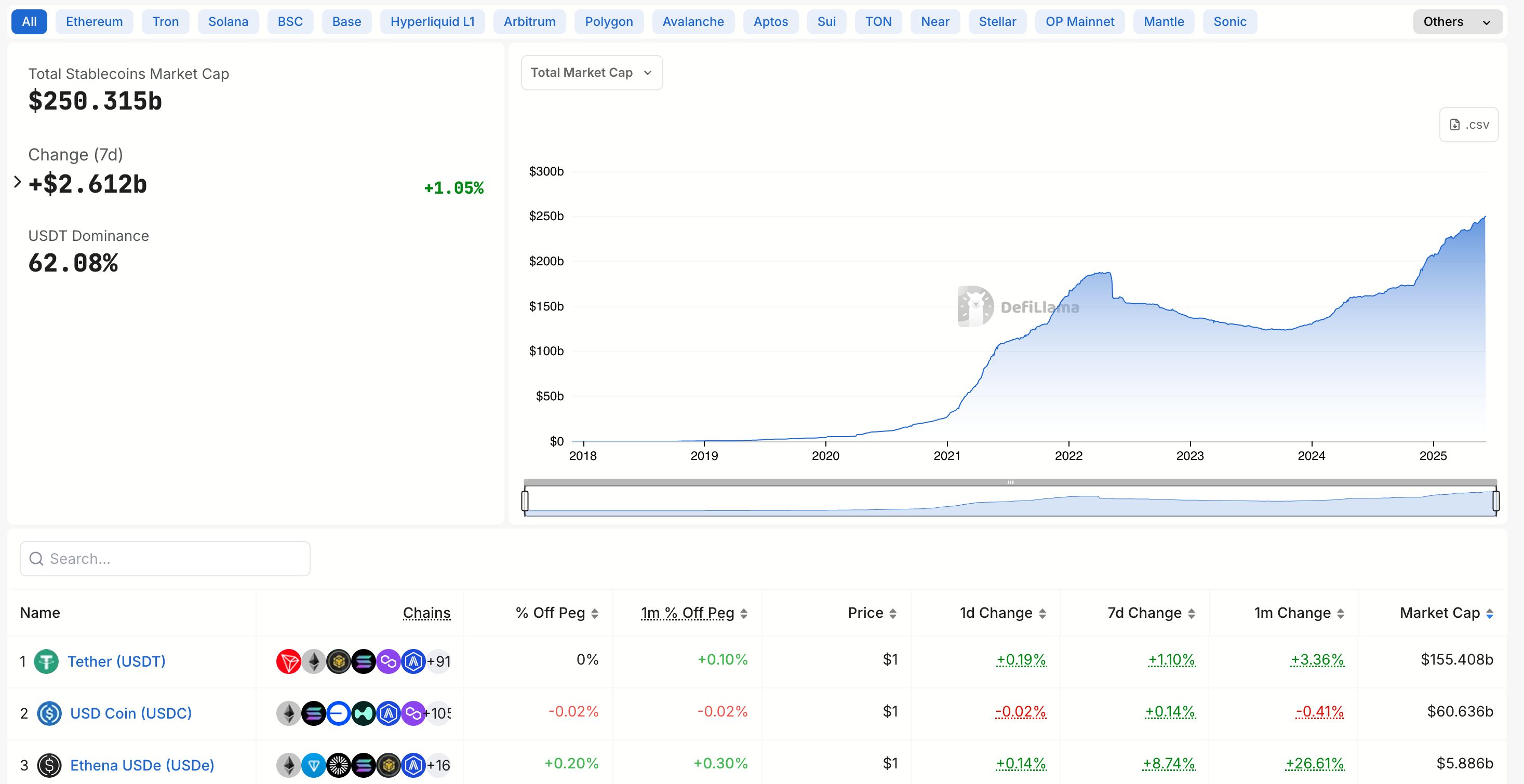

As of early June 2025, the overall stablecoin market capitalization stands impressively at approximately $250.3 billion. Tether (USDT) remains the market leader, valued around $153-154 billion, while Circle (USDC) has shown robust growth, reaching $61.05-61.5 billion, propelled by its focus on regulatory compliance. Adding to this competitive landscape, Ripple officially launched its USD-backed stablecoin, RLUSD, on December 17, 2024, aiming for enterprise-grade utility in cross-border payments and positioning itself as a key player in the evolving digital finance sector.

Beyond these dominant transactional stablecoins, yield-bearing stablecoins represent a rapidly expanding sector. By May 2025, their market capitalization surged to over $11 billion, now constituting 4.5% of the total stablecoin market. This growth, significantly driven by protocols like Ethena’s USDe and the tokenization of real-world assets (RWAs), reflects a strong demand for passive income within DeFi. The evolving global regulatory landscape, including MiCA’s implementation and proposed U.S. legislation, is set to further accelerate the mainstream and institutional adoption of all stablecoin types, driving their deeper integration into the global financial system.

Market Share and Dominance: USDT vs. USDC

The stablecoin market remains largely dominated by two giants: Tether (USDT) and Circle (USDC). As of early June 2025, the total stablecoin market value has reached approximately $250.3 billion. These two stablecoins collectively account for about 86-90% of the total market capitalization.

- Tether (USDT): USDT maintains its lead by market capitalization. As of early June 2025, its market cap is approximately $153-154 billion. While Tether reported record profits in 2024, nearing $14 billion (largely from its significant US Treasury bond holdings), its market share has seen a slight decrease, now standing at about 62.09% compared to the previous week in June 2025.

- Circle (USDC): USDC showed strong recovery and growth through 2024 and into 2025. Its market cap is approximately $61.05-61.5 billion as of June 5, 2025. Circle became the first MiCA-licensed stablecoin issuer in July 2024. This regulatory clarity is driving USDC’s adoption, particularly in regions with high remittance activity like Latin America and Southeast Asia.

Interestingly, while Tether dominates in overall market cap, data suggests USDC has been gaining traction in transaction volume on certain networks. Some reports even indicate USDC overtook Tether in stablecoin transaction volume on networks like Solana and Base by late 2024, driven by high-speed, low-cost activity.

A notable new entrant poised to challenge the established order is Ripple’s USD-backed stablecoin, RLUSD. Launched on December 17, 2024, Ripple has rapidly begun integrating RLUSD into its cross-border payment solutions, Ripple Payments.

As of early June 2025, RLUSD’s market capitalization is nearing $380 million, a significant start for a new player. Ripple aims to position RLUSD as an “enterprise-grade” and “compliant” option, leveraging its extensive network of financial institutions and existing relationships to facilitate efficient cross-border payments.

The approval of RLUSD by the Dubai Financial Services Authority (DFSA) in June 2025, allowing its use within Dubai’s financial free zone, further underscores Ripple’s strategic focus on regulatory adherence and real-world utility, setting it up as a potential challenger in the competitive stablecoin landscape.

Source: DefiLlama

The Rise of Yield-Bearing Stablecoins

The stablecoin market is currently witnessing an exciting and significant transformation with the explosive growth of yield-bearing stablecoins. These innovative assets empower users to earn passive income directly on their stable digital holdings, leveraging cutting-edge DeFi protocols or backing from real-world assets (RWAs). This shift is reshaping how investors view and utilize stable capital within the Web3 ecosystem.

By May 2025, the market capitalization of these yield-generating stablecoins surged dramatically to over $11 billion in circulation, now representing a substantial 4.5% of the total stablecoin market. This marks a steep ascent from just $1.5 billion and a mere 1% market share at the start of 2024, underscoring their rapid adoption.

The combined market cap of these assets experienced a staggering growth of over 5284% from February 2024 to February 2025. A major catalyst for this phenomenal rise is the emergence of protocols like Ethena, whose USDe asset alone crossed $3.5 billion in market cap by February 2025 and stands robustly at around $5.46 billion as of early June 2025.

Furthermore, this segment’s expansion has concurrently fueled a remarkable 414% increase in the market cap of tokenized treasury bonds. This trend powerfully highlights a growing interest in seamlessly combining the stability of digital assets with the attractive returns available from traditional financial instruments, thereby bridging the gap between conventional finance and the dynamic world of DeFi.

Evolving Landscape: Networks and Regulations

The stablecoin landscape also saw shifts in preferred blockchain networks. Ethereum and Tron’s dominance in hosting stablecoins declined from 90% to 83%. Networks like Base, Solana, Arbitrum, and Aptos captured more of this share. This shift was partly due to reduced transaction fees on Layer-2 solutions following Ethereum’s Dencun upgrade.

Furthermore, regulatory developments continue to shape the market. The pursuit of clearer frameworks, such as the EU’s MiCA, is enhancing stablecoin legitimacy. This clarity is crucial for wider institutional adoption. It also fosters trust for both traditional financial entities and governments.

The stablecoin market demonstrated robust growth and increased utility in 2024. Their transaction volumes now rival traditional payment giants. While Tether and Circle remain dominant, the emergence of yield-bearing stablecoins and shifts in network adoption signal a dynamic future. Ongoing regulatory clarity will further propel their integration into the global financial system. Investors in CRCL and other stablecoin-related assets must monitor these trends closely.

The post The Rise of Stablecoins: 2025 Market Update and Key Statistics appeared first on NFT Evening.